Commercial Real Estate: A Localized Contraction, Not a Crash

Updated Wed, Mar 25, 2026 - 11 min read

Elon Musk and others have been presaging doom within commercial real estate, though oddly enough this pessimism is not shared by the majority of experts surveyed recently by Deloitte in their 2024 Commercial Real Estate Outlook Survey. That said, there are reasons to be bearish though these negative signs do not suggest any crisis is imminent. The voices that proclaim one is looming are simply not looking closely at the facts; rather, they are reflexively reacting to how unusual the current real estate market is: In a lot of people’s minds, strange equals scary.

The commercial real estate alarmists are pointing to some real economic factors that do suggest a contraction of sorts is in the offing: However, they overstate their case and fail to consider mitigating factors. The factors most often cited are: 1) High-interest rates, 2) the work-from-home revolution, 3) e-commerce, 4) general recession fears, 5) financial pressures shared by mid-sized banks and the amount of mortgage debt turning over on office space in 2024. Let’s discuss these in more detail and then turn to a discussion of factors the pessimists are ignoring.

High interest rates

Well, there is no denying that interest rates are high and that this series of rate hikes occurred more quickly than any other in the last thirty years (though, the 2004-2006 period saw a larger total increase in the Federal Funds Rate, an increase of nearly 4% over that time). That said, when Deloitte surveyed the CEOs of major commercial real estate companies, high interest rates were only the fourth most serious concern they had—with many more ranking impending green regulation as more pressing.

Furthermore, many property owners are sitting on low-interest rate loans that they can effectively, though not literally, transfer to their new buyer by selling the property in a contract for deed deal. Contract for deed sales are essentially a rent-to-own relationship between the new buyer and the seller where the seller keeps the deed on the property while allowing the new tenant to operate and collect revenue from it, transferring the deed once the payments are completed. While single-family home sellers need cash now, owners of commercial real estate can afford to engage in this sort of arbitrage.

This means many owners of commercial real estate have a tangible financial asset they can leverage in the form of their outstanding mortgages. Furthermore, at present, the market expectation is that the Fed is more likely than not to start cutting interest rates by March of next year. Lastly, the office buildings that are most at risk, the centrally located ones in downtown areas, are the precisely the ones that are least likely to be mortgaged because they are generally older. Of course, some number of them are, but—as a whole—they are more likely to be fully owned.

The work-from-home revolution

I recently wrote an article explaining how housing affordability concerns would force employers to accept working from home, at least to some degree. That said, many workplaces are adopting a hybrid strategy. Office space vacancies, while up, have not gone up catastrophically. The NAR has the rate climbing from 12.2% to 13.3%. Companies are also taking advantage of the fact that work-from-home allows them to operate with less space to upgrade their workspaces—moving to better facilities in better locations while leasing less total space.

Let's connect, and see how we can help you stay ahead of the market.

Contact us

So, it is likely that only the less advantageous office space will be left without tenants in the new equilibrium with everyone else upgrading; however, this space can be repurposed; indeed, the low-end office space can be more readily repurposed than the high-end —being converted into retail space, even condominium units, or even stand-alone housing: All of which are in short supply. Indeed, the Deloitte Housing Survey discusses this flight to quality office space, citing this attached article.

Similarly, increased e-commerce may reduce retail demand

This is true, but—of course—e-commerce is not entirely new. Amazon has been around for nearly 30 years, having expanded beyond books well over two decades ago. However, a recent study by the ICSC entitled “The Rise of the Gen Z Consumer” reveals that the younger generation still prefers brick-and-mortar shopping. Ninety-seven percent of respondents claimed that they preferred a brick-and-mortar experience. So, if even the most internet-savvy generation prefers brick-and-mortar, it is hard to believe that e-commerce will displace it for its cost advantages.

What is more likely is that e-commerce will come to dominate certain classes of goods, namely staples (i.e., products like detergent and soap where you are buying brands you are already familiar with) and electronics while brick-and-mortar will dominate others like clothing, goods that people want to see before buying. Indeed, available retail space is below normal levels, and brick and mortar retail outlets have seen growth over the last two years while the job market remains tight meaning that consumers have purchasing power.

Furthermore, because it takes a long time to recover one’s investment in a retail space, there is a dearth of new construction going on now as investors wait to see how remote work and the e-commerce revolution play out. This means converting failing office space into retail space will offer better returns than it would if these spaces had to compete with new developments.

Recession fears

There are also fears that recession could push a commercial real estate market that is facing challenges over the edge.Of course, economic catastrophe is always possible. Indeed, some signs point to a potential recession: Deutsch Bank believes that the recent rate hikes leave the global economy susceptible to shocks, essentially if anything goes wrong, companies will not be able to “borrow their way out” as they did during the COVID-19 pandemic. This is a fair point, but even this requires an exogenous shock—Deutsch Bank’s outlook report does not point to any systemic economic imbalances like those that led to the 2008 Crisis.

“With the lagged impact of rate hikes taking effect, we can already see clear signs of data softening. In the U.S., the most recent jobs report showed the highest unemployment rate since January 2022, credit card delinquencies are at 12-year highs, and high yield defaults are comfortably off the lows,” Deutsche’s Head of Global Economics and Thematic Research, Jim Reid, and Group Chief Economist David Folkerts-Landau said in their latest report.

Recent indicators

That said, recent indicators—like the difference between the 3-month and 10-year treasury yield (i.e. how close we are to yield curve inversion)—have tipped below the 50% mark in recent months according to Statista and, more importantly, we remain at above full employment (economists consider 5% unemployment the natural rate, i.e. full employment, as the economy requires people to move between jobs as part of its normal functioning). Unless the employment situation changes considerably, a serious recession is impossible—and there is quite a bit of slack in the unemployment rope: If there is a recession, it will not be a catastrophic one.

The main economic risk is that banks had failed to properly hedge against duration risk and that this would cause a collapse of the US financial sector (i.e. a reduction in the value of their T-bills and other bonds, which are normally considered “safe”) has clearly passed: Even the least diligent risk officers should have adopted some way of dealing with this by now, and with inflation falling we can assume the worst of the rate hikes are behind us.

Coming from small and mid-sized banks

Lending to commercial real estate developers and managers largely comes from small and mid-sized banks, where the pressure on liquidity has been most severe. Furthermore, a considerable portion of commercial real estate debt is coming due in 2024. About 80% of all bank loans for commercial properties come from regional banks. Pessimists believe banks are likely to pull back on commercial real estate commitments more rapidly in a world where they’re more focused on liquidity.

That said, even a cash-strapped regional bank would prefer to refinance a loan on favorable terms than to see the loan default. However, it is important to keep in mind that this definition of “small and mid-sized banks” refers to institutions with “a pittance of 250 billion dollars in assets.” Given the equity cushion offered by larger down payments on commercial real estate loans, these institutions are a little more robust than George Bailey’s savings and loan from “It’s a Wonderful Life.”

Now that we have discussed the factors commercial real estate pessimists point to, let’s consider some positive signs that I haven’t managed to mention yet:

Reshoring in the aftermath of Covid-19

The supply chain disruptions experienced during the COVID-19 pandemic which resulted from various countries’ different responses to the crisis have made many American companies invest in fully domestic production processes. This, in turn, means increased demand for industrial real estate, a section of the real estate market most of the pessimistic articles coming out simply ignore. This sector will continue to see robust growth, offsetting some of the downturns experienced in the office sector. Of course, many real estate companies do not hold any real estate in this category, so individual firms still remain exposed to risk—but this silver lining should not be ignored. The following article provides some empirical support for the reshoring narrative.

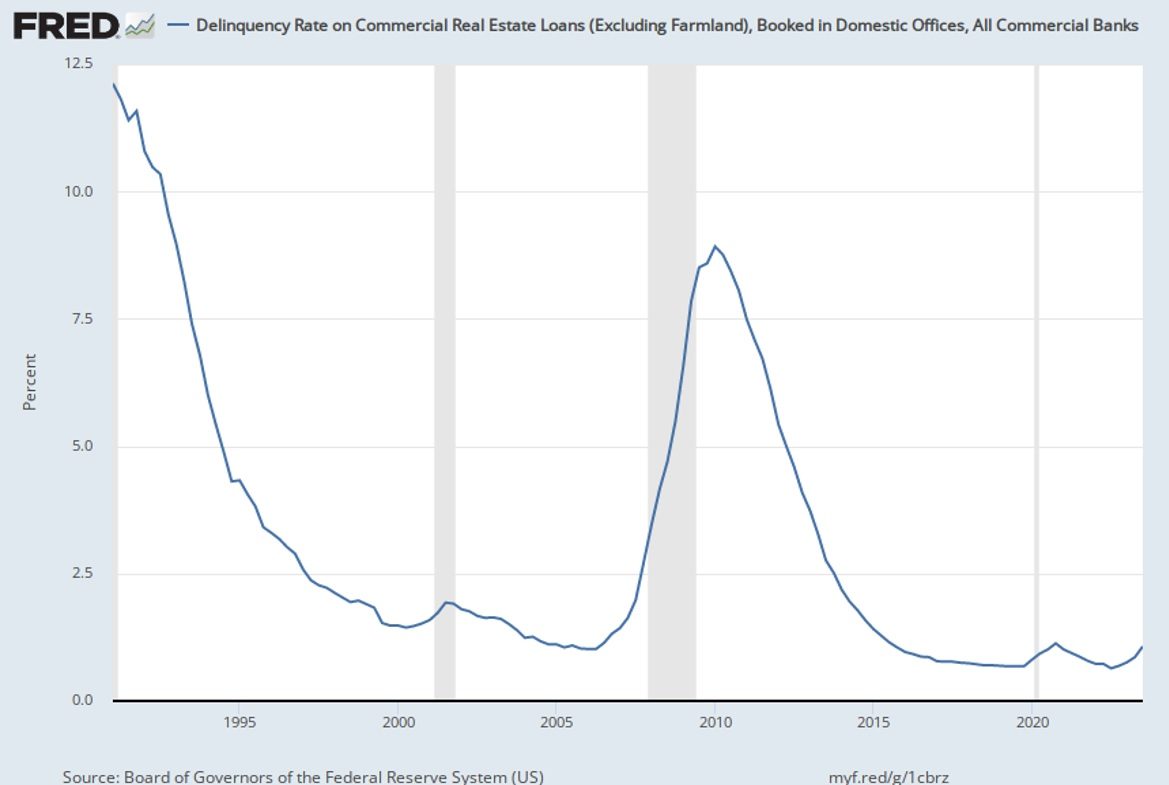

Mortgage foreclosures are still low

By historical standards (even if Mezzanine loans, essentially bridge loans commercial real estate companies take out are at record highs, these “highs” are still in the range of 66 loans total). As you can see below, delinquencies on commercial real estate loans are well below what they were throughout the 90s: A decade that I remember quite fondly and that by almost all measures was a time of economic prosperity. Of course, they were similarly low going into the crisis, but during the Crisis of 2008 there was more going on—namely weak employment numbers and huge amounts of bad single family mortgage debt. Commercial real estate can obviously be affected by a recession or depression, but there are no examples of it being the leading cause of one: The position of Elon Musk and the other Chicken Littles.

The role of the NAR

The NAR has noted that universities are showing an interest in leasing office space to attract students back to class. In major cities, where office space is likely to take the biggest hit and where conversion is the most difficult, this could help to shore up flagging demand—even if it is not an overwhelming factor.

Read more: NAR force Zillow change business model

Meanwhile, apartment rents are either steady or increasing in most markets

Meaning that developers of multifamily units should also be willing to buy out holders of underperforming office buildings. A significant portion of those offices can be converted into apartments.

Banks are continuing to make commercial real estate loans though it is decelerating somewhat

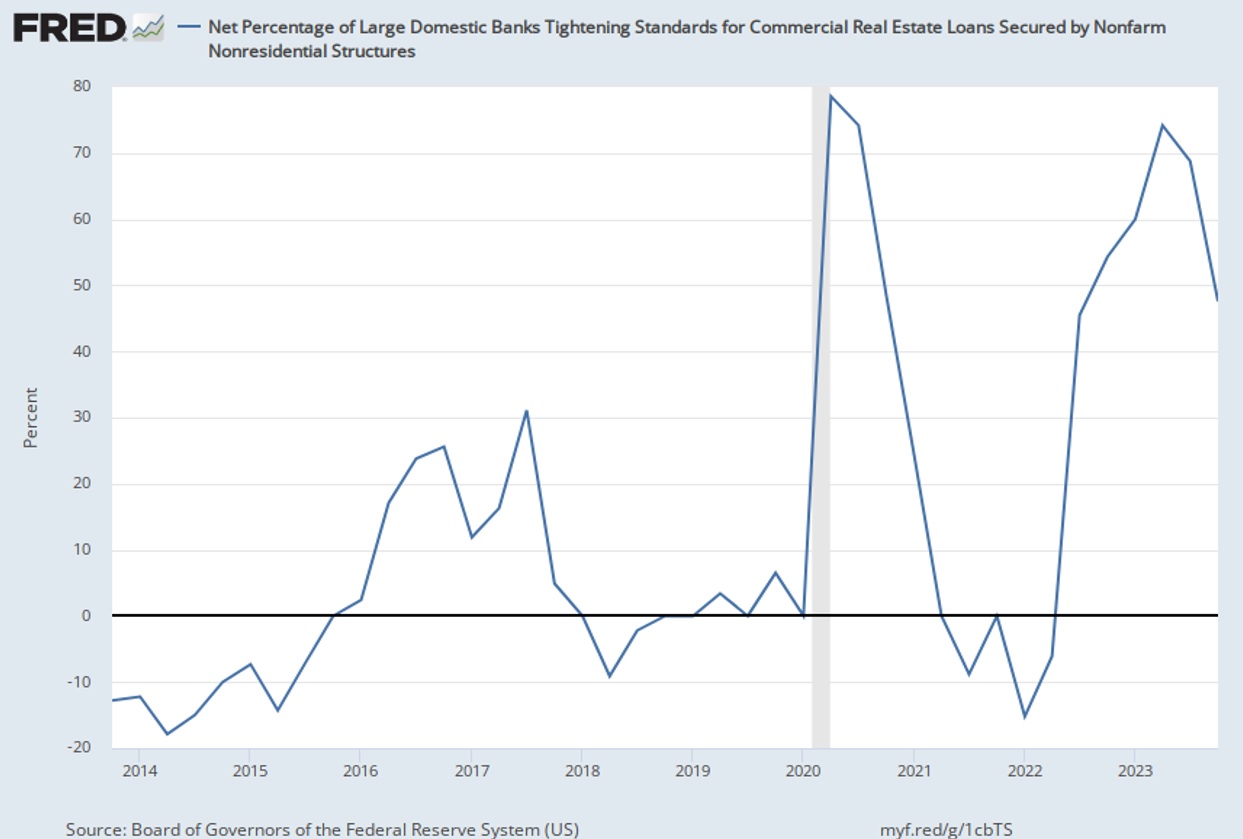

Furthermore, it looks like we have already turned a corner on the tightening of lending standards:

New office building construction in city centers is at a low

In previous booms, construction activity increased going into the bursting of a bubble—with construction activity declining only after a crisis began. Here the absence of newly built supply suggests that regular population pressures will eventually reflate the market even if work from home reduces demand in the short run.

While there is reason to be concerned about the office sector of commercial real estate, the fear that it will set off a major recession is overblown. In fact, there has never been a recession caused by a bust in the commercial real estate sector. Some claim the 1990-1991 recession was caused by this, but most people believe it was caused by the shock to oil production resulting from Saddam’s invasion of Kuwait and the subsequent Gulf War.

The outstanding debt on commercial real estate loans are a fraction of outstanding debt on single-family mortgages even when we include apartments: And office buildings are just a fraction of that fraction, roughly 25% of the outstanding commercial real estate debt. Furthermore, commercial loans require much larger down payments than single-family mortgages do—meaning that you must see considerable depreciation before a property owner would think it better to default on his loan than to just sell his property.

Conclusion

Those who are panicking about commercial real estate simply have not acquainted themselves with the numbers involved. If commercial real estate causes a recession, it will be a minor one, but a soft landing both for the economy and the commercial real estate sector generally seem much more likely. That said, if you do invest in commercial real estate, I would stay away from buying office space unless you have both incredible local knowledge and profound reasons to do so. The other sectors, esp. the industrial sector, are likely to continue performing well and will likely offset the losses in the office space sector.

Read more: NAR and MBA send Fannie a letter

Franklin Carroll

Franklin Carroll is Kukun's VP of Modelling and Analytics; After finishing his studies at the University of Chicago, he worked at Fannie Mae where he helped build Collateral Underwriter, roll out the Value Verify initiative, and specialized in collateral related and credit related policy.

Published December 12, 2023