The “End Hedge Fund Control of American Homes Act” Is Seriously Misguided

Updated Wed, Aug 21, 2024 - 8 min read

The “End Hedge Fund Control of American Homes Act” is as dangerous as the bill’s name is misleading: Hedge funds do not control American homes; indeed, they are a minority of total single-family real estate investment, in terms of both homes bought and dollars spent. The bill, seeking to make amendments to the Internal Revenue Code of 1986, introduces a punitive excise tax on certain taxpayers who fail to liquidate their single-family real estate holdings.

While legislation aimed at addressing the housing shortage is much needed, singling out large institutional investors is, frankly, little more than scapegoating. In fact, by denying access to rental units to families that are unable to afford a mortgage and effectively banning most alternative ways of funding a home purchase, this legislation promises to make the housing market even more dysfunctional than it currently is.

Understanding the Legislation

At the core of the bill is Chapter 50B, a new addition to the tax code, which would impose a 50% tax on the “fair market value” of newly acquired single-family residences for applicable taxpayers, ramping up over the next ten years when it would finally take full effect. Section 5000F, however, takes a different route by penalizing those who fail to meet specific requirements related to excess single-family residences by imposing a hefty $50,000 fine for each residence over a specified limit. Rules regulating what constitutes an “excess” are stipulated in Section 5000G.

Section 5000G defines terms, establishes aggregation rules, and mandates reporting to the Secretary while outlining penalties for non-compliance. Meanwhile, Section 3 introduces a housing down-payment Trust Fund, funded by the imposed taxes, which is then earmarked for down-payment assistance grants.

Of course, the legislation is extremely vague. It does not outline who exactly will qualify for this down-payment assistance. That said, these tax penalties are so Draconian that there will likely be no meaningful amount of money ever placed in this fund. The legislation is effectively a government ban on companies owning more than fifty houses of single-family real estate masquerading as a tax.

The Legislation and Taxation

The legislation places a fifty-thousand-dollar tax on homes owned by hedge funds—allowing them to go untaxed on 90% of the number of homes they currently own in the first year, 80% the second year, etc. until eventually all homes are taxed. Similarly, it applies a nearly identical tax on all other large holders of single-family properties—with the exception that these entities are allowed to own fifty homes, with the “excess” applying only to the number of homes owned over fifty. After ten years, this 50,000 dollar per home tax would be replaced by a tax of 50% of the home’s “fair market value.” In the long run, this would be tantamount to instituting a fifty-home cap on all single-family real estate investors.

Let's connect, and see how we can help you stay ahead of the market.

Contact us

The bill does, luckily, exempt banks holding foreclosed homes and builders whose properties are not currently leased to anyone: Without these exceptions, the bill could accidentally trigger a banking crisis or prevent nearly all new single-family housing construction. That said, its effects on the housing market would, on net, be harmful. Indeed, given its current wording, the bill perversely incentivizes hedge funds speculating in single-family real estate to hold onto their properties without renting them because unoccupied properties are not subject to the confiscatory 50% tax.

Speculations Around The Legislation

Of course, speculating on increasing property values by buying and holding the land without leasing it to tenants will only reduce the supply of housing still further. A policy that leaves perfectly fine homes unoccupied is an inherently inefficient one. Of course, there are reasons to save assets for future use, but an asset like housing can often depreciate faster when it is not occupied as issues with the property go unnoticed and worsen.

Many of the articles complaining about the “problem of hedge fund speculation” point out that many hedge funds are buying property in minority neighborhoods. This means that the proposed legislation could have the unintended effect of denying people who live in these areas access to single-family rentals: The smaller landlords that the legislation favors are more likely than larger landlords to engage in red-lining, simply because it is harder to prove in the case of smaller land-holders—just as it is harder to prove racial bias in the case of smaller employers. (Just so you know, I have nothing against small businesses and believe the vast majority are owned by good, fair people. I see both large and small businesses as playing a valuable role in the economy. My point is only about provability.) Many families living in these areas find themselves, at least temporarily, unable to afford a mortgage and need access to these rental properties.

Read more: Speculation in the home flipping market

Alternative Financing and The Problem of Title Theory States

The way the legislation is currently worded, it would ban large-scale rent to own and equity sharing financing. It essentially discourages any sort of innovation in the financing space that would require a large company to own stakes in properties—at least temporarily. Furthermore, the way the bill is currently worded, it makes an exception for large scale land holders under only the following circumstances:

(A) a mortgage note holder that owns a single-family residence through foreclosure,

(B) a organization which is described in section 501(c)(3) and exempt from tax under section 501(a),

(C) any person primarily engaged in the construction or rehabilitation of single-family residences, or

(D) any person who owns federally subsidized housing.

Notice that these exceptions do not include businesses involved in equity sharing agreements or rent to own arrangements. Moreover, it does not make an exception for mortgage lenders, or other institutions, that own property in title theory states. For those who are not familiar, there are two kinds of mortgages—those that rely on title theory and those that rely on lien theory. In a title theory state, the bank, or some institution tasked with holding the title for the bank, holds the title until the loan is fully paid at which point ownership is transferred to the borrower.

In a lien theory state, on the other hand, the owner holds title and the bank must make a claim for that title if he fails to pay. Technically speaking, this bill would prevent mortgage lending in title theory states (which, ironically enough, includes Virginia, Maryland, and the District of Columbia where many of those proposing this legislation own homes—in addition to the tiny state of California among others). This is a glaring hole in the legislation that would produce a serious market failure unless the courts take immediate corrective action.

Hedge Funds Are Not the Cause of the Affordability Crisis

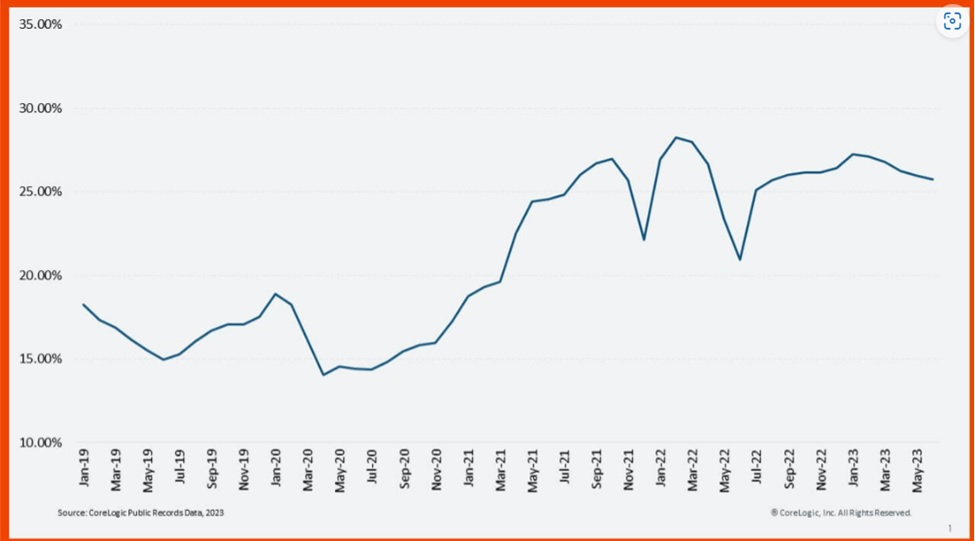

Hedge funds make up only a fraction of investment purchasers. And investment purchases, while high by historical standards (though they are off their 2022 peak), still constitute only a fraction of all home purchases.

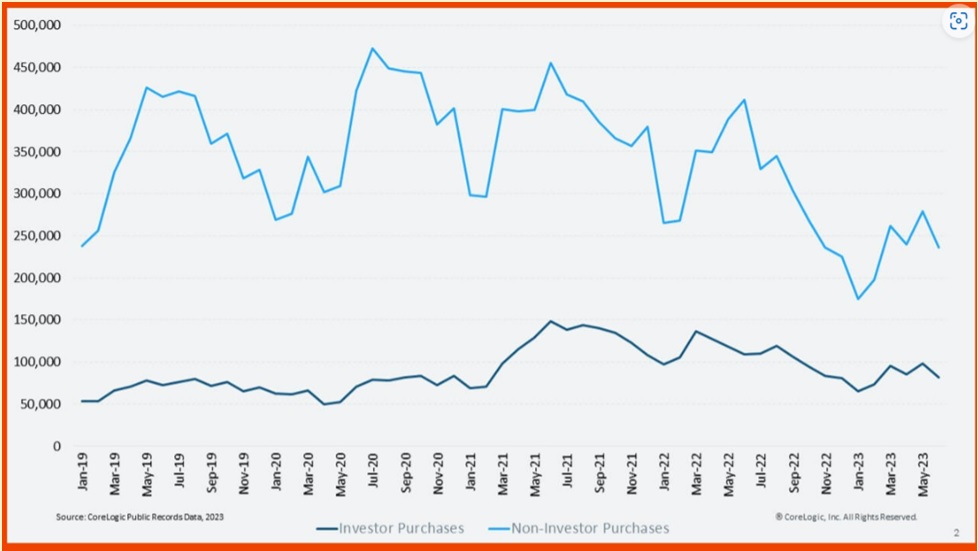

Housing supply and demand have fallen together—as the locked-in effect makes homeowners unwilling to sell and high interest rates make buyers unable to buy: Indeed, the decision to sell your home and buy a new one is, in the current market, effectively a decision to refinance into a massively higher interest rate. In absolute terms, investor activity is also down, as the following graph illustrates.

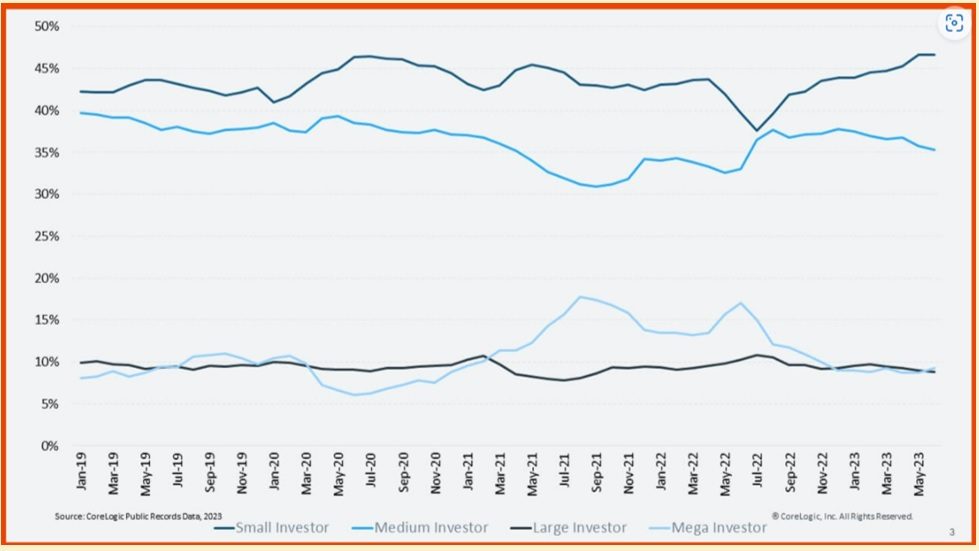

If mega-investors are pricing out regular buyers, why aren’t they also pricing out smaller investors? Small investors make up a larger percentage of investment purchases, while the mega-investors have become a smaller one. It is hard to believe that an actor who is reducing its activity in the market is somehow responsible for the affordability crisis. Furthermore, why blame the hedge funds? Wouldn’t it make sense to blame medium and small investors? They not only make up a larger share of the investor market, but they are also the ones increasing their market share, not the hedge funds.

Conclusion

The real drivers of the affordability crisis are 1) high interest rates and 2) limitations on new construction—with limitations on new construction being the more long-standing, and more important, cause. Interest rates will eventually come down, but we have no reason to believe that building new homes will become any easier as time goes on. Of course, local governments benefit from lower populations and elevated home prices as they seek to maximize per capita revenue: This perverse incentive must be dealt with if housing is ever to become affordable again. (See my article on housing affordability.)

The “End Hedge Fund Control of American Homes Act” is a fundamentally misguided piece of legislation. While the legislation may be well-meaning, in reality, it simply scapegoats institutional investors and reduces the available stock of single-family, standalone rental housing. It will only make the problem worse.

Read more: Doing away with title insurance requirements

Franklin Carroll

Franklin Carroll is Kukun's VP of Modelling and Analytics; After finishing his studies at the University of Chicago, he worked at Fannie Mae where he helped build Collateral Underwriter, roll out the Value Verify initiative, and specialized in collateral related and credit related policy.

Published December 21, 2023