Elevating Home Value with the PICO™ Home Condition Score

Updated Wed, Jun 25, 2025 - 6 min read

Homeowners and lenders alike know that a property’s condition has a material impact on its market value and lending risk. Yet “condition” often remains opaque in public records or automated valuations. Kukun’s PICO™ Home Condition Score brings transparency: akin to a credit score for homes, PICO ranges from 500 (teardown/land only) to 850 (brand-new construction), reflecting the useful life of key systems and finishes. The GSEs and the appraisal industry rank the condition of any property from C1 to C6.

However, not all parts are treated equally. For example, a roof that is 15 years old is good. We would not necessarily say the same thing about windows or the kitchen. The PICO was built to age out every component of the house and leverage the permit data to zero the clock on some of those components.

Thus, when someone renovates a part of the house, the condition score will reflect it. By updating renovations and repairs in the PICO model, homeowners see how condition-driven changes translate to a higher score, and thus a stronger valuation. Lenders and insurers can leverage PICO to refine risk assessments and engage clients on proactive home maintenance.

Why Condition Matters: Evidence from Research

Research confirms that property condition significantly influences sale price, especially when a home is notably better or worse than neighborhood norms. A study of over 300,000 U.S. home sales found that including condition metrics in valuation models yields more accurate pricing and highlights value differences in weaker markets or in homes that stand out in quality or deterioration. Moreover, Kukun’s cost estimator and ROI, which leverages AI models to forecast value after renovations, clearly demonstrate that certain projects can add a lot of value (equity) to a house while others add modest values or even none. Value reports show that targeted updates, like a minor kitchen remodel and visible projects, can deliver value increases that compound market value over time.

How PICO™ Works

- Useful Life & Depreciation Logic: PICO’s score is a detailed understanding of “useful life.” For example, HVAC systems typically have a 15-year lifespan, kitchens and bathrooms 25–30 years, and roofs often around 20–25 years, depending on materials. When homeowners update these items, PICO credits them as if new; if updates are older, PICO applies depreciation algorithms and comparable data to estimate their remaining value.

- User-Driven Updates: Homeowners and appraisers answer simple questions about recent renovations and repairs (e.g., “When was the roof last replaced?” “Have you updated HVAC, Kitchen, Bathrooms?”). These updates take only a minute but can raise the PICO score above what public records reflect.

- Valuation Link: Kukun’s proprietary valuation model translates PICO into an adjusted market value. For instance, a home with a base automated valuation may be undervalued if its condition updates aren’t in public data; updating PICO can reveal that the true market value is higher.

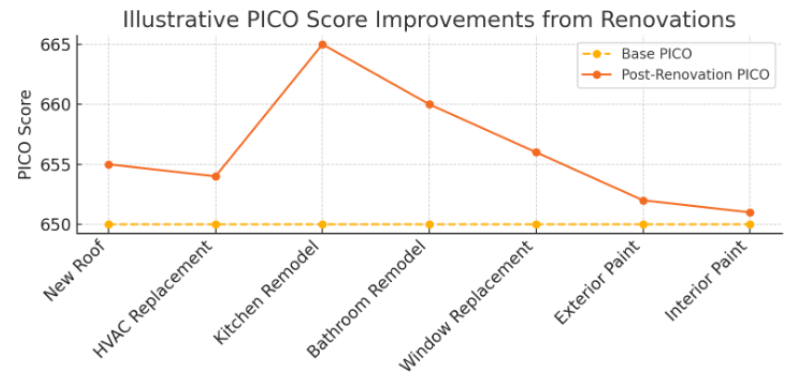

- Illustrative Example: (See charts above.) For a hypothetical $300,000 home at a base PICO of 650, replacing elements like roof, HVAC, kitchen, or bathroom can raise PICO points proportionally. The illustrative chart shows, for example, a kitchen remodel (cost $30K; estimated value bump $22K based on national recoup data) could lift PICO and drive a higher valuation. While actual PICO algorithms are more granular and more intelligent, this example highlights the concept: targeted updates yield measurable condition score improvements and value uplift.

Benefits for Homeowners

- More Accurate Home Valuation: Homeowners learn their “true” home equity by reflecting completed renovations and repairs, not just aging public records.

- Informed Decision-Making: By modeling “future value” scenarios (e.g., “If I replace windows now, how much could my value rise?”), Homeowners can prioritize updates that offer the best condition improvement and ROI.

- Access to Financing: A higher PICO-backed valuation can support refinancing, HELOCs, or sale pricing decisions by demonstrating up-to-date condition to lenders or buyers.

- Maintenance Planning: PICO highlights near-term maintenance needs (e.g., HVAC nearing end of useful life), helping homeowners budget proactively and avoid costly emergency repairs.

Benefits for Lenders, Insurers, and Brokers

- Refined Risk & Pricing: Banks can incorporate PICO into underwriting models to gauge collateral strength more accurately. Homes with higher condition scores pose lower maintenance risk, potentially justifying better terms.

- Engagement & Cross-Sell: Lenders can prompt clients to update their PICO before refinancing or applying for a home-equity product, engaging them in home maintenance conversations, and positioning the institution as a trusted advisor.

- Portfolio Insights: Aggregated PICO data across a lender’s portfolio can reveal geographic patterns of aging systems, guiding product offerings (e.g., targeted renovation loan promotions in areas with older housing stock).

- Digital Experience: Through Kukun’s white-label integration (API or iframe), institutions can embed PICO assessment tools directly in their online portals. Homeowners enter recent updates, immediately see a revised score and valuation, and then explore financing options.

- Competitive Differentiation: Offering a transparent condition score boosts customer loyalty by showing that the lender cares about preserving and enhancing home value, not merely closing loans.

Fact-Checked Context & Data

- Condition’s Impact: A large-scale study on U.S. home sales (2012–2015) found that quality differences matter more when markets weaken, underscoring the condition’s role in price stability and risk assessment.

- Renovation ROI: Remodeling magazine’s 2024 Cost vs. Value report shows exterior projects like garage door replacement can recoup nearly 194% of cost, entry door 188%, and a minor kitchen remodel around 96% nationally. One thing to note is that expensive and luxurious finish-level material will have less impact on ROI. These data illustrate how specific updates translate to value additions that PICO captures.

- Home Equity & Financing: As homeowners sit on record equity, reflecting true home condition becomes crucial for lenders to offer appropriate products.

Integration & Next Steps

Kukun’s PICO™ Home Condition Score is available as a white-label solution, easily integrated via API or iframe into lender and real estate platforms. Institutions can configure branding, capturing homeowner inputs on renovations in a seamless UX. The backend leverages Kukun’s extensive data to compute scores and updated valuations instantly. For a personalized demo or to learn more about integrating PICO™, visit Kukun PICO Score or contact our team.

Let's connect, and see how we can help you stay ahead of the market.

Contact us

Raf Howery

Raf Howery is the founder and CEO of Kukun. Howery, a self-professed "serial renovator" and entrepreneur, started Kukun to transform the home remodeling industry from an offline, fragmented, and frustrating undertaking to an online, modern, and user-friendly experience.

Published June 25, 2025