Homeowners keep remodeling despite higher interest rates

Updated Mon, Jun 23, 2025 - 6 min read

People love their homes, and they love to make their homes better. With the clean, uncluttered, light & bright interior styles that are so popular nowadays, most older homes feel dated. It only takes a visit to a friend’s house to see the magic of a transformed kitchen or bathroom, which creates the spark of motivation to do the same. People describe feelings of their home making them happy just by walking into a room and that they suddenly want to entertain more often.

Home remodeling is growing across the country at a fast pace despite high-interest rates, inflation, and concerns of possible economic downturn.

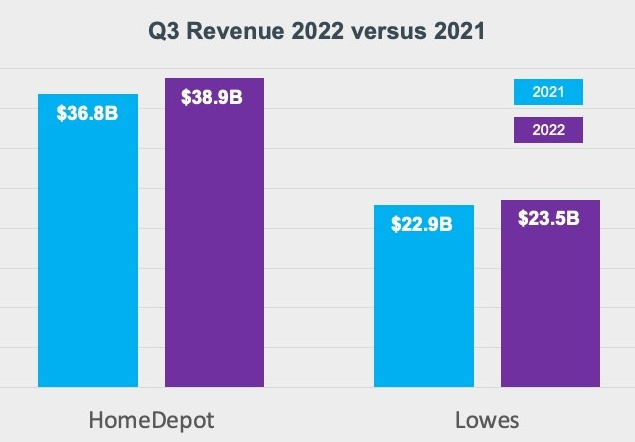

You may think this is counterintuitive, but more than 50% of all homeowners in 2022 have completed at least one remodeling project. And more money has been spent overall on remodeling in 2022 versus 2021. Home Depot and Lowes are the best indicators of the pace of home remodeling and repair. They are both up in 2022 versus 2021 – which is significant given the frenzy of work people were putting into their homes last year.

One complicating factor with the data is that inflation and supply chain price swings make the year-on-year comparison more of a directional indication rather than a precise measure of activity. That’s because, in 2021, the supply chain limitations drove enormous price increases in many items, notably wood, which went up over 200%. Now wood is back down to pre-pandemic price levels; however, inflation has impacted other things, so while supply chain price spikes are not as much of a factor, they are at least partially offset by inflation.

Why is remodeling so resilient in a high-interest-rate environment?

When interest rates are low and home prices are rising, as they have been over the last several years, remodeling is seen to be very affordable. That’s because homeowners can get cash-out refinancing, where the cash covers the cost of their home improvement, and the lower interest rate can make the new payment a negligible difference. It’s an investment, a real investment, that will increase the value of your home and enable you to turn your house into your dream home.

And people who are thinking of selling are motivated to remodel so they can get a higher sales price. Most of the time, homeowners in a good economy have both the “dream home investment” and “maximized sales price” rationale.

When interest rates go up, fewer people think about selling their house and moving to a new one. Instead, they want to hang on to their low fixed-rate mortgage, so they focus on “improving in place.” Once people decide to do a significant remodel, they are so thrilled with the results that they feel like they got the new home they wanted and can’t imagine selling. It’s an investment of time and emotion with a payoff of a style and comfort that they want to enjoy for years.

Let's connect, and see how we can help you stay ahead of the market.

Contact us

Home remodeling is a wise investment after several years of rapid home price appreciation.

When home prices accelerate, the home’s new higher value provides more opportunity for equity financing, and the home value can support and payout a high-quality remodel. Rising home prices often move homes up the quality scale – which means you can justify a higher level of quality in kitchen cabinets, counters, fixtures, and even appliances.

Every home has a minimum required quality for remodels – this means that home buyers expect a certain level of quality in all the finishes. In a multi-million-dollar home, for example, you will actually reduce the value of the house if you put in 69 cents per square foot discount linoleum flooring.

On the other hand, every home has a high range for remodeling investment recoupment. These are finishes like custom cabinets and premium branded fixtures that are seen as a good match for the price range of the home. So, when there are several years of home price appreciation, a home that previously wouldn’t warrant premium finishes now does.

Homeowners love this; they can justify luxurious remodels because it pays out or comes closer to paying out. Pair that with the equity available for financing, and you have a recipe for home improvements.

At Kukun, we provide the industry’s leading Renovation Cost Calculator for free

You can easily create different scenarios and design your project. It provides the expected ROI from your remodel as well. Try it at mykukun.com/Home-Renovation-Costs.

Financing remodels with home equity loans is extremely popular

Most people borrow against their home equity to finance home improvements because, despite the cost of borrowing, they are better off financially in the long run. Banks report that more than 55% of all home loans are used for home improvement. Today fewer people are financing home improvements by refinancing their mortgage; instead, they are turning to Home Equity Loans and HELOCs, which have become the home improvement financing option of choice.

There are two kinds of loans:

- Home Equity Loan – A lump sum borrowed on a fixed interest rate with a defined term for repayment.

- Home Equity Line of Credit, also known as HELOC – Allows homeowners to borrow on an as-needed basis, up to a specific limit. HELOCs typically have a variable interest rate.

Some people are more comfortable with a fixed interest rate they get with a home equity loan and the set term for the loan to be repaid. Other people prefer the flexibility of the HELOC, only taking out a bit at a time and potentially not taking out the total amount of the loan.

Popular projects homeowners can’t get enough of

Home investment typically comes in two forms – updating the décor and repairs.

When it comes to updates, kitchens and bathrooms are always popular as it just takes a new coat of paint throughout the house and updated Kitchen and Bathrooms to make your home feel like a new house. Another popular update is flooring, as there are new materials like engineered hardwoods, LVT (Luxury vinyl tile), LVP (Luxury vinyl plank), and more that are affordable, durable, and look great.

Repairs include:

- Installing a new roof.

- Replacing the heating and air conditioning systems.

- Miscellaneous plumbing and electrical fixes

But don’t just replace what was there originally – instead, combine energy-efficient upgrades with repairs to cut your utility bills, particularly now that energy prices are incredibly high. Some of these improvements include dual pane windows, high-efficiency heating, air conditioning, water heaters, appliances, and even solar roofs and solar roof panels. These items cost a bit more up-front to install, but they pay back over time in savings.

Nervous about home prices potentially falling?

Home prices are softening a little in some markets, flat in other markets, and prices are still going up in other markets. Most economists don’t expect to see drastic home price reductions as overall inflation and a dramatic housing shortage are expected to keep prices from tumbling. The result is that most home values are likely to stay very high compared with pre-pandemic levels, which means one thing – it’s time for that dream renovation you’ve always wanted!

Read more: Driving HELOC conversions

Scott Langmack

Scott Langmack is the COO at Kukun, an AI-powered Property Technology platform. With decades of experience in general management and marketing in the tech industry, he's passionate about innovation in technology for real estate. Before Kukun, he founded companies in cloud recruitment and Fintech. Scott also has extensive global leadership experience with top brands like Microsoft and Pepsi-Cola. He's an angel investor in companies like Lending Club and Credible. Scott holds an MBA from USC and enjoys designing houses, mountain biking, skiing, tennis, and hiking.

Published August 20, 2023