Blog Guides Lending and mortgage

How Much Equity Do I Have in My Home? 2026 Guide

Updated Wed, Jan 14, 2026 - 19 min read

Top blog articles

What is Home Equity? The Complete Definition

Simple Definition:

Home equity is the portion of your home that you truly own. It’s the difference between your home’s current market value and what you owe on all mortgages secured by the property.

Formula: Home Equity = Current Market Value – Total Mortgage Debt

Real Example:

- Home value: $450,000

- First mortgage: $280,000

- HELOC balance: $20,000

- Home Equity = $450,000 – $300,000 = $150,000

Why Home Equity Matters:

1. Financial Net Worth

- Home equity is typically the largest component of net worth for most Americans

- Average homeowner equity: $300,000 (Q4 2025)

- Total US homeowner equity: $32 trillion

2. Borrowing Power

- Can borrow 75-90% of available equity

- Lower interest rates than credit cards/personal loans

- Tax-deductible if used for home improvements

3. Retirement Asset

- Can be accessed via reverse mortgage (62+)

- Downsizing releases equity for retirement income

- Home equity makes up 40-50% of retiree net worth

4. Funding Home Improvements

- Kitchen remodel: $25K-$80K → Adds $30K-$100K value

- Bathroom renovation: $15K-$40K → Adds $20K-$55K value

- HVAC replacement: $8K-$15K → Adds $10K-$20K value [Link to Cost Estimator for each]

How to Calculate Your Home Equity: 5-Step Process

Step 1: Determine Your Home’s Current Market Value

4 Methods to Value Your Home:

Method 1: Online Home Value Estimator (Instant, Free)

- Zillow Zestimate: ±5-10% accuracy

- Redfin Estimate: ±5-10% accuracy

- Kukun AVM: ±3-8% accuracy (more precise)

- Best for: Quick estimate

- Cost: Free

- [Get Your Home Value Estimate] (CTA to Kukun tool)

Method 2: Comparative Market Analysis (CMA) by Agent (1-3 days, Free)

- Real estate agent analyzes recent comparable sales

- Adjusts for differences (size, condition, features)

- More accurate than online estimators (±3-5%)

- Best for: Considering selling soon

- Cost: Free (agents provide, hoping to list your home)

Method 3: Professional Appraisal (7-10 days, $400-$600)

- A licensed appraiser physically inspects the home

- Most accurate valuation (±0-3%)

- Required for refinancing, HELOCs, and home equity loans

- Best for: Applying for a loan or an accurate value needed

- Cost: $400-$600

Method 4: Broker Price Opinion (BPO) (3-5 days, $75-$150)

- Real estate broker provides a written valuation

- Less detailed than an appraisal

- Used by lenders for some loan types

- Best for: Middle ground between CMA and appraisal

- Cost: $75-$150

Regional Home Value Variations:

- San Francisco Bay Area: Median $1.2M (high equity opportunity)

- New York Metro: Median $650K

- Seattle Metro: Median $780K

- National Median: $420K

- Rural areas: Median $280K

Step 2: Calculate All Mortgage Debt

Include ALL Liens on Your Property:

First Mortgage:

- Find the current balance on the most recent statement

- Or call the lender for the exact payoff amount

- Use payoff amount (includes interest), not statement balance

Second Mortgage (if any):

- Some homeowners have piggyback loans (80-10-10, 80-15-5)

- Include full balance

Home Equity Line of Credit (HELOC) (if any):

- Include the current balance owed

- Even if in the draw period

Home Equity Loan (if any):

- Include the remaining balance

Other Liens:

- Tax liens (unpaid property taxes)

- Mechanic’s liens (unpaid contractors)

- Judgment liens (court-ordered debts)

Example Calculation:

- First mortgage: $285,000

- HELOC balance: $35,000

- Total debt: $320,000

Step 3: Calculate Your Home Equity

Simple Subtraction:

Home Equity = Market Value – Total Mortgage Debt

Example 1: Positive Equity (Most Common)

- Home value: $500,000

- Total mortgages: $320,000

- Home equity: $180,000 (36% equity)

Example 2: High Equity (Owned Long Time)

- Home value: $650,000

- Total mortgages: $120,000

- Home equity: $530,000 (82% equity)

Example 3: Low Equity (Recently Purchased)

- Home value: $400,000

- Total mortgages: $380,000

- Home equity: $20,000 (5% equity)

Example 4: Negative Equity / Underwater (Rare in 2026)

- Home value: $350,000

- Total mortgages: $380,000

- Home equity: -$30,000 (underwater by $30K)

Step 4: Calculate Your Loan-to-Value (LTV) Ratio

LTV Formula:

LTV = (Total Mortgage Debt ÷ Home Value) × 100

Example:

- Total mortgages: $320,000

- Home value: $500,000

- LTV = ($320,000 ÷ $500,000) × 100 = 64%

What LTV Means:LTV Ratio What It Means Borrowing Potential 0-50% Excellent equity position Can borrow heavily, best rates 51-70% Good equity position Can borrow, good rates 71-80% Moderate equity Can borrow, standard rates 81-95% Low equity Limited borrowing, higher rates 96-100% Minimal equity Very limited borrowing >100% Underwater/negative equity Cannot borrow, refinance difficult

Why LTV Matters to Lenders:

- Lower LTV = lower risk = better loan terms

- Most lenders max LTV at 80-90% for HELOCs/HELs

- PMI required if LTV >80% on purchase/refinance

- FHA allows up to 96.5% LTV

- VA allows 100% LTV (no down payment)

Step 5: Calculate How Much You Can Borrow

Tappable Equity Formula:

Tappable Equity = (Home Value × Maximum LTV) – Total Mortgage Debt

Most lenders allow 80-90% combined LTV (CLTV) for HELOCs and home equity loans.

Example Calculation (80% Max LTV):

- Home value: $500,000

- Maximum 80% LTV: $500,000 × 0.80 = $400,000

- Current mortgages: $320,000

- Tappable equity: $400,000 – $320,000 = $80,000

Example Calculation (90% Max LTV):

- Home value: $500,000

- Maximum 90% LTV: $500,000 × 0.90 = $450,000

- Current mortgages: $320,000

- Tappable equity: $450,000 – $320,000 = $130,000

Factors That Affect How Much You Can Borrow:

- Credit score: 740+ gets best terms, 620+ minimum usually

- Debt-to-income ratio: <43% preferred

- Employment history: 2+ years of stable employment

- Income: Must qualify for monthly payments

- Home condition: Poor condition reduces borrowing (PICO Score!)

Your Home’s PICO Score Directly Impacts Available Equity

Critical Insight Most Homeowners Miss:

Your home’s condition doesn’t just affect market value—it affects how much a lender will LET you borrow against your equity.

The PICO Score Connection

What is PICO Score? PICO (Property Intelligence for Condition Optimization) is a 0-100 score that measures your home’s physical condition based on:

- System age & functionality (HVAC, roof, plumbing, electrical)

- Interior condition (kitchen, bathrooms, flooring, paint)

- Exterior condition (siding, windows, foundation, landscaping)

- Maintenance history

- Building permits & improvements

How PICO Score Affects Available Equity

Poor Condition (PICO 40-60):

- ❌ Appraisal comes in 5-12% below market estimate

- ❌ Lenders reduce max LTV to 70-75% (vs. 80-90% for good condition)

- ❌ Higher interest rates (+0.5-1.5%)

- ❌ May require repairs before loan approval

Example:

- Estimated home value: $500,000

- PICO Score: 52/100 (poor condition)

- Actual appraisal: $460,000 (8% below estimate)

- Max 75% LTV: $345,000

- Current mortgage: $320,000

- Available to borrow: $25,000 (vs. $80K with good condition!)

Good Condition (PICO 70-85):

- ✅ Appraisal at or near market value

- ✅ Standard max LTV (80-85%)

- ✅ Competitive interest rates

- ✅ Smooth approval process

Example:

- Estimated home value: $500,000

- PICO Score: 78/100 (good condition)

- Actual appraisal: $505,000 (at market)

- Max 80% LTV: $404,000

- Current mortgage: $320,000

- Available to borrow: $84,000

Excellent Condition (PICO 86-100):

- ✅ Appraisal often above market estimate

- ✅ Maximum LTV available (85-90%)

- ✅ Best interest rates

- ✅ Lender confidence is high

Example:

- Estimated home value: $500,000

- PICO Score: 92/100 (excellent condition)

- Actual appraisal: $520,000 (4% above estimate)

- Max 85% LTV: $442,000

- Current mortgage: $320,000

- Available to borrow: $122,000

Condition Impact Summary:

- Poor condition (PICO 52): $25K available

- Good condition (PICO 78): $84K available

- Excellent condition (PICO 92): $122K available

- Difference: $97,000 in borrowing power!

Check Your Home’s PICO Score Now

Which Home Systems Affect PICO Score Most

Critical Systems (Highest Impact):

1. HVAC System (Age & Functionality)

- System >15 years: -8-15 PICO points

- Non-functional system: -15-25 PICO points

- Impact on equity: Reduces appraisal $8K-$20K

- Solution: HVAC replacement $6K-$15K → Increases equity $10K-$25K

2. Roof Condition

- Roof >20 years: -10-18 PICO points

- Missing shingles/leaks: -15-25 PICO points

- Impact on equity: Reduces appraisal $10K-$30K

- Solution: Roof replacement $8K-$25K → Increases equity $15K-$40K

3. Kitchen Condition

- Outdated kitchen (20+ years): -8-15 PICO points

- Non-functional appliances: -10-20 PICO points

- Impact on equity: Reduces appraisal $15K-$40K

- Solution: Kitchen remodel $25K-$80K → Increases equity $30K-$100K

4. Bathroom Condition

- Outdated bathroom(s): -5-10 PICO points per bathroom

- Plumbing issues: -8-15 PICO points

- Impact on equity: Reduces appraisal $8K-$25K

- Solution: Bathroom renovation $15K-$40K → Increases equity $20K-$55K

5. Foundation & Structure

- Foundation cracks: -15-30 PICO points

- Water damage: -10-25 PICO points

- Impact on equity: Reduces appraisal $15K-$60K

- Solution: Foundation repairs $5K-$30K → Preserves/increases equity

The Smart Strategy: Use Equity to Fund Improvements That Increase Equity

The Concept:

You can borrow against your equity to make improvements that increase your home’s value MORE than the borrowed amount, creating a positive equity loop.

The Equity Growth Strategy

Starting Position:

- Home value: $450,000

- Mortgage: $280,000

- Home equity: $170,000

- Available to borrow (80% LTV): $80,000

- PICO Score: 58/100 (fair condition)

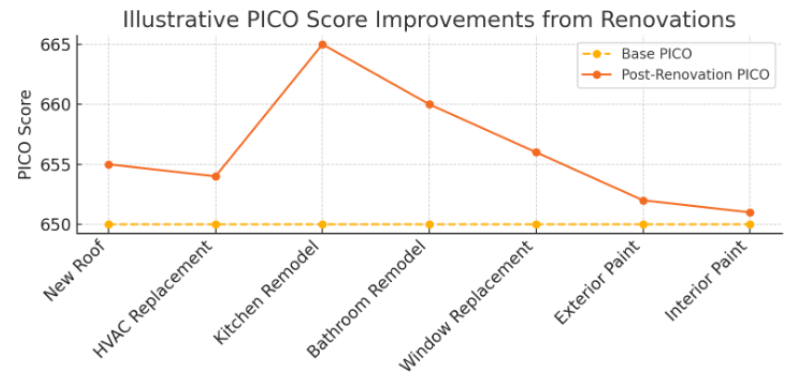

Strategic Improvements Plan ($60,000 borrowed via HELOC):

Improvement 1: Kitchen Remodel – $35,000

- New cabinets, countertops, appliances, and flooring

- Value add: $45,000-$55,000

- ROI: 129-157%

- PICO impact: +15-20 points

Improvement 2: Master Bathroom Renovation – $15,000

- New vanity, tile, fixtures, lighting

- Value add: $20,000-$25,000

- ROI: 133-167%

- PICO impact: +8-12 points

Improvement 3: HVAC Replacement – $10,000

- Replace 20-year-old system

- Value add: $12,000-$18,000

- ROI: 120-180%

- PICO impact: +12-15 points

Total Investment: $60,000 (borrowed via HELOC at 8% = $400/mo interest-only)

New Position (After Improvements):

- Home value: $527,000 ($450K + $77K value add)

- Total mortgage: $340,000 ($280K + $60K HELOC)

- New home equity: $187,000 (vs. $170K before)

- New PICO Score: 83/100 (vs. 58 before)

- Equity increase: $17,000 (even after borrowing $60K!)

Plus Additional Benefits:

- Better appraisal ($527K vs $435K if hadn’t improved)

- More available to borrow in future

- Faster sale when ready (buyers want move-in ready)

- Monthly energy savings ($150-$300 from new HVAC)

Net Financial Impact:

- Invested: $60,000 (borrowed)

- Value added: $77,000

- Equity gained: $17,000

- Monthly cost: $400 interest-only (8%)

- Monthly savings: $200 (energy)

- Net monthly cost: $200

- Can rent out basement for $1,200/month → Net $1,000 positive cash flow!

Calculate ROI for Your Home Improvements

Top 10 Improvements That Increase Equity Most

Ranked by ROI:

1. Minor Kitchen Remodel – 85-95% ROI ⭐⭐⭐⭐⭐

- Cost: $25,000-$35,000

- Value add: $30,000-$50,000

- Equity gain: $5,000-$15,000

- PICO impact: +15-20 points

2. Bathroom Addition (2nd or 3rd bathroom) – 80-100% ROI ⭐⭐⭐⭐⭐

- Cost: $20,000-$40,000

- Value add: $25,000-$60,000

- Equity gain: $5,000-$20,000

- PICO impact: +20-30 points

3. Bathroom Remodel – 70-80% ROI ⭐⭐⭐⭐⭐

- Cost: $15,000-$25,000

- Value add: $18,000-$35,000

- Equity gain: $3,000-$10,000

- PICO impact: +10-15 points

4. HVAC Replacement – 70-90% ROI ⭐⭐⭐⭐⭐

- Cost: $8,000-$15,000

- Value add: $10,000-$22,000

- Equity gain: $2,000-$7,000

- PICO impact: +12-18 points (if old system)

5. Roof Replacement – 60-75% ROI ⭐⭐⭐⭐

- Cost: $10,000-$25,000

- Value add: $12,000-$30,000

- Equity gain: $2,000-$5,000

- PICO impact: +10-15 points (if old roof)

6. Siding Replacement – 60-70% ROI ⭐⭐⭐⭐

- Cost: $8,000-$20,000

- Value add: $10,000-$25,000

- Equity gain: $2,000-$5,000

- PICO impact: +8-12 points

7. Window Replacement – 65-75% ROI ⭐⭐⭐⭐

- Cost: $8,000-$18,000

- Value add: $10,000-$22,000

- Equity gain: $2,000-$4,000

- PICO impact: +8-12 points

8. Deck Addition – 65-80% ROI ⭐⭐⭐⭐

- Cost: $10,000-$20,000

- Value add: $12,000-$24,000

- Equity gain: $2,000-$4,000

- PICO impact: +5-8 points

9. Flooring Replacement – 60-75% ROI ⭐⭐⭐⭐

- Cost: $6,000-$15,000

- Value add: $8,000-$18,000

- Equity gain: $2,000-$3,000

- PICO impact: +5-10 points

10. Basement Finishing – 60-75% ROI ⭐⭐⭐⭐

- Cost: $30,000-$75,000

- Value add: $35,000-$85,000

- Equity gain: $5,000-$10,000

- PICO impact: +15-25 points

Explore All Home Improvement Costs & ROI

5 Ways to Tap Your Home Equity (With Pros, Cons & Costs)

Method 1: Home Equity Line of Credit (HELOC)

What it is: Revolving credit line (like credit card) secured by your home

How it works:

- Draw period: 5-10 years (borrow, repay, borrow again)

- Repayment period: 10-20 years (pay off remaining balance)

- Interest: Variable rate (currently 7-10%)

- Monthly payment: Interest-only during draw period

Maximum Amount: Up to 85-90% CLTV

- Example: $500K home, $300K mortgage → Can access $125K-$150K

Costs:

- Application fee: $0-$500

- Closing costs: $0-$1,000 (often waived)

- Annual fee: $0-$100

- Interest rate: Prime + 0.5-2% (currently 7-10%)

Pros:

- ✅ Only borrow what you need

- ✅ Pay interest only on the amount used

- ✅ Can borrow again after repaying

- ✅ Interest may be tax-deductible (if used for home improvements)

- ✅ No penalties for early repayment

Cons:

- ❌ Variable interest rate (can increase)

- ❌ Risk of overspending (too easy to access)

- ❌ Home is collateral (risk foreclosure if can’t pay)

- ❌ Rates higher than first mortgages

Best for:

- Multiple home improvement projects over time

- Ongoing funding needs

- People with discipline (won’t overspend)

- Don’t want to pay interest on unused funds

Current Rates (January 2026): 7.5-9.5%

Method 2: Home Equity Loan (HEL)

What it is: Fixed-rate, lump-sum loan secured by your home (second mortgage)

How it works:

- Borrow a lump sum upfront

- Fixed interest rate

- Fixed monthly payments (principal + interest)

- Typical term: 5-30 years (commonly 10-20 years)

Maximum Amount: Up to 85-90% CLTV

Costs:

- Application fee: $0-$500

- Closing costs: $500-$2,000 (2-5% of loan amount)

- Appraisal: $400-$600

- Interest rate: 7.5-11% (fixed)

Pros:

- ✅ Fixed interest rate (predictable payments)

- ✅ Fixed monthly payment (easier budgeting)

- ✅ All funds available immediately

- ✅ Interest may be tax-deductible (home improvements)

- ✅ Lower rates than personal loans/credit cards

Cons:

- ❌ Must borrow full amount (pay interest on entire sum)

- ❌ Can’t borrow more later without new loan

- ❌ Closing costs higher than HELOC

- ❌ Home is collateral

Best for:

- One-time large expense (single renovation)

- Want predictable fixed payments

- Interest rate stability important

- Specific project budget known upfront

Current Rates (January 2026): 8-10.5%

Example Payment:

- Loan amount: $50,000

- Rate: 9%

- Term: 15 years

- Monthly payment: $507

- Total interest paid: $41,260

Method 3: Cash-Out Refinance

What it is: Replace existing mortgage with larger mortgage, receive difference in cash

How it works:

- New mortgage replaces old mortgage

- Borrow more than you owe, receive difference

- Single loan (not second mortgage)

- Fixed rate, new term (typically 30 years)

Maximum Amount: Up to 80% LTV (sometimes 85-90% with good credit)

Example:

- Home value: $500,000

- Current mortgage: $300,000

- Cash-out refinance: $400,000 (80% LTV)

- Cash received: $100,000 (minus closing costs)

Costs:

- Closing costs: 2-5% of new loan amount ($8,000-$20,000 on $400K loan)

- Appraisal: $400-$600

- Title insurance: $1,000-$3,000

- Interest rate: 6.5-8%

Pros:

- ✅ Lowest interest rate (first mortgage rates)

- ✅ Single monthly payment (no second loan)

- ✅ Can extend term (lower monthly payment)

- ✅ May lower rate if rates have dropped

- ✅ Interest tax-deductible (if used for home improvements)

Cons:

- ❌ High closing costs ($8K-$20K)

- ❌ Resets mortgage term (back to 30 years)

- ❌ Only makes sense if current rate high or need large amount

- ❌ Longer approval process (30-45 days)

Best for:

- Current mortgage rate significantly higher than today’s rates

- Need large amount ($75K+)

- Want single payment (not second mortgage)

- Can afford higher monthly payment (if rate similar)

Current Rates (January 2026): 6.5-7.5%

When Cash-Out Refi Makes Sense:

- Current mortgage rate: 8%+

- Today’s rate: 7% or less

- Benefit: Lower rate + access equity

When It Doesn’t:

- Current mortgage rate: <6.5%

- Today’s rate: 7%+

- Problem: Would increase rate just to access cash

Method 4: Reverse Mortgage (Age 62+)

What it is: Loan that pays YOU based on your home equity (no monthly payments)

How it works:

- For homeowners 62+ years old

- Lender pays you (lump sum, monthly, or line of credit)

- No monthly payments required

- Loan repaid when you move, sell, or pass away

Maximum Amount:

- Varies by age (older = higher percentage)

- Typical: 40-60% of home value

- Example: $500K home → $200K-$300K available

Costs:

- Origination fee: $2,500-$6,000

- Closing costs: $2,000-$5,000

- Mortgage insurance: 2% upfront + 0.5% annually

- Interest rate: 6-9%

Pros:

- ✅ No monthly payments (loan balance grows)

- ✅ Can stay in home for life

- ✅ Flexible payout options

- ✅ Non-recourse loan (won’t owe more than home worth)

Cons:

- ❌ Loan balance grows over time (reduces inheritance)

- ❌ High fees (5-6% of home value)

- ❌ Must maintain home, pay taxes/insurance

- ❌ Heirs must repay or sell home

Best for:

- Seniors 62+ with significant equity

- Want to age in place

- Need retirement income

- No plans to leave home to heirs

Current Rates: 6.5-8.5%

Method 5: Sell and Downsize

What it is: Sell current home, buy smaller/less expensive home, keep the difference

How it works:

- Sell home for $500,000

- Pay off $300,000 mortgage

- Buy new home for $350,000

- Keep $150,000 (minus selling costs ~$30K = $120K cash)

Costs:

- Realtor commission: 5-6% ($25K-$30K on $500K)

- Closing costs: 1-3% ($5K-$15K)

- Moving costs: $2K-$5K

- Total: $32K-$50K

Pros:

- ✅ Access ALL equity

- ✅ No monthly loan payments

- ✅ Lower property taxes (smaller home)

- ✅ Lower maintenance/utilities

- ✅ No debt

Cons:

- ❌ Must move (leave neighborhood/home)

- ❌ High transaction costs (5-8%)

- ❌ Disruption to life

- ❌ May not find a suitable smaller home in the same area

Best for:

- Empty nesters (kids moved out)

- Want to retire debt-free

- Ready to downsize lifestyle

- Smaller home meets needs

10 Ways to Build Home Equity Faster

1. Make Extra Principal Payments

How it works:

- Pay more than the required monthly payment

- Extra goes directly to principal reduction

- Reduces interest paid, builds equity faster

Example:

- Mortgage: $300,000 at 7%, 30 years

- Required payment: $1,996/month

- Pay extra: $500/month ($2,496 total)

- Result: Paid off in 17 years (vs. 30), save $187K interest, built equity 13 years faster

Best strategy:

- One extra payment per year: Reduces 30-year mortgage to 26 years

- Bi-weekly payments (26 half-payments = 13 full payments/year): Reduces to 23-25 years

2. Home Value Appreciation (Market-Driven)

Average home appreciation:

- Historical average: 3-5% per year

- Hot markets: 8-15% per year (2021-2022)

- Current (2026): 4-6% per year (normalized)

Example:

- Home value: $400,000

- 5% annual appreciation

- After 5 years: $510,000 (+$110,000 equity from appreciation)

- After 10 years: $652,000 (+$252,000 equity from appreciation)

Regional variations:

- San Francisco Bay Area: 6-10%/year

- Seattle, Denver, Austin: 5-8%/year

- National average: 4-6%/year

- Declining areas: 0-2%/year

How to maximize:

- Buy in appreciating neighborhoods

- Check building permit trends (active construction = appreciation) [Check Building Permits Near You]

3. Strategic Home Improvements

High-ROI improvements build equity:

- Kitchen remodel: 85-95% ROI → $5K-$15K equity gain

- Bathroom addition: 80-100% ROI → $5K-$20K equity gain

- HVAC replacement: 70-90% ROI → $2K-$7K equity gain

4. Improve Your PICO Score

How condition affects equity:

- Low PICO (40-60): Reduces appraisal 5-12%

- High PICO (75-90): Appraisal at or above market

Priority improvements:

- Replace aging HVAC (>15 years): +12-18 PICO points

- Replace old roof (>20 years): +10-15 PICO points

- Update outdated kitchen: +15-20 PICO points

- Renovate dated bathrooms: +10-15 PICO points

5. Refinance to Shorter Term

30-year to 15-year refinance:

- Builds equity 2x faster

- Saves massive interest ($100K+ on $300K mortgage)

- Higher monthly payment (but more goes to principal)

Example:

- Mortgage: $300,000 at 7%

- 30-year payment: $1,996/month (paid off 2056)

- 15-year payment: $2,696/month (paid off 2041)

- Extra cost: $700/month

- Benefit: $187,000 less interest, paid off 15 years sooner

6. Avoid Taking Out Second Mortgages (or Pay Them Off)

Every dollar borrowed reduces equity:

- HELOC borrowed: -$50K equity

- Home equity loan: -$40K equity

- Total debt: +$90K, Equity reduced by $90K

Strategy:

- Only borrow for value-add improvements

- Pay off HELOCs/HELs as quickly as possible

- Avoid using equity for depreciating assets (cars, boats)

7. Make a Larger Down Payment (If Buying)

Higher down payment = more immediate equity:

- 5% down ($400K home): $20K equity (95% LTV)

- 20% down ($400K home): $80K equity (80% LTV)

- 30% down ($400K home): $120K equity (70% LTV)

Benefits:

- More equity from day 1

- No PMI required (20%+ down)

- Lower monthly payments

- Better loan rates

8. Pay Off Mortgage Faster with Lump Sum Payments

Use windfalls to build equity:

- Tax refund: $3,000-$8,000

- Work bonus: $5,000-$20,000

- Inheritance: Variable

- Side business profit: Variable

Impact of $10K lump sum:

- $300K mortgage, 7%, 30 years

- Make $10K payment in Year 1

- Result: Mortgage paid off 2 years sooner, save $17K interest

9. Increase Home Value Through Curb Appeal

Low-cost, high-return improvements:

- Professional landscaping: $1,000-$3,000 → Adds $5,000-$15,000 value

- Fresh exterior paint: $3,000-$8,000 → Adds $8,000-$20,000 value

- New front door: $800-$2,500 → Adds $3,000-$8,000 value

- Outdoor lighting: $500-$2,000 → Adds $2,000-$6,000 value

10. Maintain Your Home (Prevent Value Loss)

Deferred maintenance reduces value:

- Roof leak ignored: -$10,000-$30,000 value (water damage spreads)

- HVAC failure ignored: -$8,000-$15,000 value

- Foundation crack ignored: -$15,000-$50,000 value

Regular maintenance preserves equity:

- Annual HVAC service: $150-$300

- Gutter cleaning: $100-$200

- Roof inspection: $150-$300

- Prevents costly repairs, maintains value

Home Equity FAQS (15 Questions)

1. What is a good amount of home equity to have?

A good amount of home equity is 20% or more of your home’s value. This eliminates PMI and provides borrowing flexibility. Ideal: 30-50% equity (provides cushion against market downturns).

Example: $400K home → Good equity: $80K+ (20%), Ideal: $120K-$200K (30-50%)

2. How long does it take to build home equity?

On a 30-year mortgage with 20% down, you’ll have approximately:

- 5 years: 25-28% equity

- 10 years: 35-40% equity

- 15 years: 50-55% equity

- 20 years: 65-75% equity

Accelerate with extra payments, appreciation, or strategic improvements.

3. What happens to my home equity when I sell?

Your home equity becomes cash at closing:

- Sale price: $500,000

- Mortgage payoff: $280,000

- Selling costs (6-8%): $30,000-$40,000

- Net proceeds: $460,000-$470,000

This is YOUR money (tax-free up to $250K single, $500K married for primary residence).

4. Can I lose home equity?

Yes, home equity can decrease due to:

- Market decline (home values drop)

- Taking out new loans (HELOC, home equity loan)

- Neglecting maintenance (reduces home value)

- Negative amortization loans (rare)

Protect equity by maintaining home, avoiding unnecessary borrowing, and making principal payments.

5. How does a HELOC affect my credit score?

HELOCs impact credit in 3 ways:

- Credit inquiry: -5-10 points (temporary)

- Credit utilization: Using >30% of HELOC hurts score

- Payment history: On-time payments help, late payments hurt significantly

Best practice: Use <30% of available HELOC limit, pay on time.

6. Can I still access my equity if I have bad credit?

Limited options with poor credit (<620):

- HELOCs: Difficult (most require 680+ credit)

- Home equity loans: May qualify at 620+ (higher rates)

- Cash-out refinance: FHA allows 580+ credit (higher costs)

- Sell and downsize: No credit check required

Strategy: Improve credit first (6-12 months), then access equity at better rates.

7. What is negative equity (being underwater)?

Negative equity occurs when you owe more on your mortgage than your home is worth.

Example:

- Home value: $350,000

- Mortgage balance: $380,000

- Negative equity: -$30,000

Causes: Market decline, low down payment, taking out second mortgages

Solutions: Continue paying, wait for appreciation, principal reduction, strategic default (extreme cases)

8. How does property condition affect available equity?

Poor condition reduces appraisal 5-12%, limiting borrowing:

- Low PICO Score (40-60): Max 70-75% LTV (vs. 80-85% good condition)

- Appraisal reductions: $15,000-$50,000 typical

- Lender may require repairs before approval

Solution: Check PICO Score, make strategic improvements before applying for equity loans.

9. Should I use home equity to pay off debt?

Pros:

- Lower interest rate (7-9% vs. 18-28% credit cards)

- Tax-deductible interest (if used for home improvements)

- Single monthly payment

Cons:

- Home becomes collateral (risk foreclosure)

- Converts unsecured debt to secured debt

- May extend repayment period

- Doesn’t address spending habits

Best for: High-interest debt ($20K+), stable income, spending habits under control

10. How much equity do I need to eliminate PMI?

You need 20% equity (80% LTV) to eliminate PMI on conventional loans.

Example:

- Home value: $400,000

- Mortgage: $320,000

- Equity: $80,000 (20%) → Can request PMI removal

Process:

- Reach 20% equity (pay down or appreciation)

- Request new appraisal ($400-$600)

- If appraisal confirms 80% LTV, lender removes PMI

- Save $100-$300/month (typical PMI cost)

11. Can I borrow against equity if I’m retired?

Yes, with sufficient income to qualify:

- HELOC/HEL: Must show income (pension, Social Security, investments)

- Reverse mortgage: Age 62+, NO income requirement, NO monthly payments

- Cash-out refi: Requires qualifying income

Best option for retirees: Reverse mortgage (no income requirement, no payments)

12. How does home equity differ from home value?

- Home value: What your home is worth on the market ($500,000)

- Home equity: What YOU own ($500,000 value – $300,000 mortgage = $200,000 equity)

You can have a high-value home with low equity (if you recently purchased) or low-value home with high equity (if owned long time, low mortgage).

13. What happens to home equity in a divorce?

Home equity is typically divided based on:

- Community property states: 50/50 split

- Equitable distribution states: “Fair” split (not always 50/50)

Options:

- Sell home, split proceeds

- One spouse buys out the other’s equity share

- One spouse keeps the home, other gets different assets

Example buyout:

- Home value: $500,000

- Equity: $200,000

- One spouse keeps the home, pays the other $100,000 (50% of equity)

14. Does home equity count as income?

No, home equity is NOT income. It’s an asset (net worth).

However:

- Borrowing against equity: NOT income (it’s a loan)

- Selling home: Gain may be income, BUT excluded if:

- Primary residence

- Owned 2+ years

- Gain <$250K (single) or <$500K (married)

15. How often should I check my home equity?

Check home equity:

- Annually: General awareness

- Before major purchase: (car, college, etc.) to assess borrowing capacity

- Before refinancing: To calculate LTV, available cash-out

- If considering selling: To project net proceeds

- After market changes: Up or down >10%

Equity in America: Key Statistics [2026]

Average Home Equity by Age:

- Under 35: $25,000-$75,000 (recent purchasers)

- 35-44: $100,000-$150,000

- 45-54: $175,000-$250,000

- 55-64: $250,000-$350,000

- 65+: $350,000-$450,000

Average Home Equity by Region:

- West: $425,000 (highest – CA, WA, OR)

- Northeast: $275,000

- South: $200,000

- Midwest: $175,000

Total U.S. Homeowner Equity: $32 trillion (Q4 2025)

Homeowners with:

- 50%+ equity: 68% of homeowners

- 20-50% equity: 24%

- <20% equity: 6%

- Negative equity: 2% (historically low)

Home Equity Access (2025):

- HELOCs outstanding: $420 billion

- Home equity loans: $280 billion

- Cash-out refinances: $125 billion

Average HELOC balance: $65,000

Average home equity loan: $45,000

Written by Ramona Sinha. July 29, 2020

Ramona is the Senior Content Writer for Kukun. This experienced blogger uses simple and succinct words to decipher the complex phenomenon called life. She has written articles covering a broad range of topics, such as real estate, lending and mortgage, finance, business, taxation, home designs, home improvement projects, decor concepts, and more. An avid traveler, she’s a digital nomad at heart and an animal lover from the depth of her soul.

Top blog posts

See more >

Recommended

Join our newsletter

Get helpful renovation tips, insightful home maintenance articles, real estate market trends, and more.

Please enter a name

Please enter a valid e-mail