Blog Guides Lending and mortgage

How to Get a Pool Loan: A Practical Guide to Financing Your Backyard Pool

Updated Tue, Jun 2, 2026 - 8 min read

Top blog articles

A backyard pool sounds like a straightforward purchase until you start getting contractor quotes. The average inground pool now costs $66,000 nationally – up 72% since 2019, according to Pool Corp.’s 2024 data – and that number doesn’t count the deck, fencing, lighting, or heater. Most homeowners don’t have that sitting in savings. Pool loans exist specifically to bridge that gap, but they’re not all the same, and choosing the wrong one can cost you thousands in extra interest over a 7-year term.

This guide walks you through what to expect at every step: how to size your budget, which loan type fits your situation, what lenders actually look for, and how to apply without getting caught off guard.

What Does a Pool Actually Cost?

Before you talk to a single lender, you need a real number. “I want a pool” isn’t a loan application. A contractor quote is.

Inground pools nationally average $66,000, with most projects landing between $44,500 and $87,500 depending on pool size, material (fiberglass vs. concrete vs. vinyl liner), and your region (Pool Corp., 2024). Above-ground pools are a different category entirely – they run $1,000-$6,000 and rarely require financing. If you’re reading this, you’re probably thinking inground.

Here’s where budgets slip: the pool shell is just the beginning. Add-ons, including decking, fencing, a heater, lighting, and landscaping, routinely push the final project cost $10,000-$20,000 over the base quote. Annual ownership – chemicals, electricity, cleaning, and repairs – runs another $3,000-$6,000 per year according to Bankrate’s pool financing data. That ongoing cost matters when you’re calculating how much monthly loan payment you can actually absorb.

When you start comparing financing paths, resources that explain how to get a pool loan in detail, including how lenders size loan amounts against project costs, can help you figure out whether your quote is in a fundable range before you ever submit an application.

Get two or three contractor quotes before you approach any lender. The spread between the lowest and highest bid on the same pool can easily be $10,000-$15,000. Know what the job actually costs.

Your Pool Financing Options, Explained

Three loan types handle most pool projects. They’re not interchangeable. Which one suits you depends on your credit score, how much equity you have in your home, and how much risk you’re willing to take on.

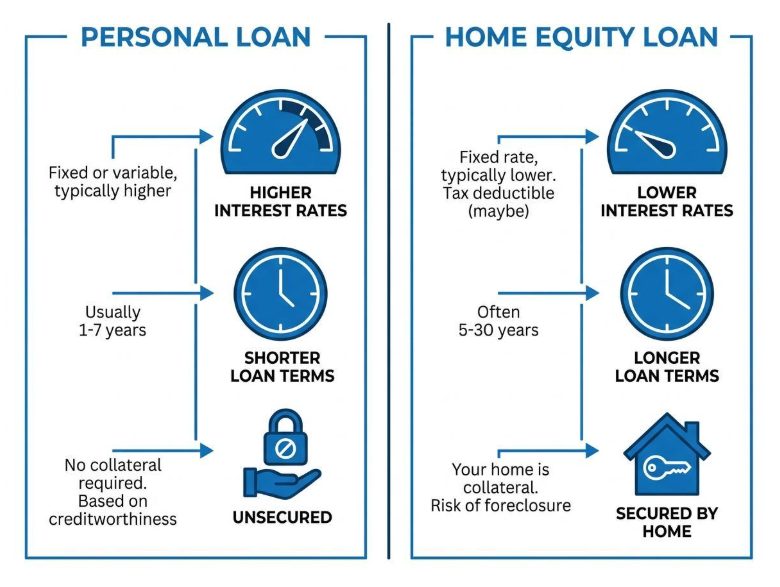

- Personal loans are unsecured – your home isn’t collateral. They’re faster to close (sometimes funded within a day or two), typically cap at $50,000-$100,000 depending on the lender, and carry terms from 2 to 7 years. The tradeoff is rate: personal loan APRs range from 6% to 36%, and where you land on that spread depends almost entirely on your credit score. For borrowers who don’t have much home equity or don’t want to risk their house, personal loans are often the right call.

- Home equity loans work differently. You borrow against the equity you’ve built in your home, get a fixed rate (often starting around 8% for qualified borrowers), and can spread repayment over up to 30 years. That longer term means a lower monthly payment, but it also means more total interest paid and your home is on the line if things go sideways.

- HELOCs, or home equity lines of credit, offer a draw period of roughly 10 years where you pull funds as needed, then a repayment phase of 15-20 years. The variable rate is the catch: it’s linked to market benchmarks and can climb, which makes budgeting harder.

One more option worth knowing about: dealer or contractor financing offered at the point of sale. It’s convenient, but the rates are usually higher than what you’d find shopping independently. Don’t accept it without comparing.

For more on how pool loans overlap with broader renovation financing, our deck loans and home renovation financing guide covers how lenders assess these projects.

How to Qualify for a Pool Loan

Your credit score drives almost everything here. It determines which loan types you can access and what rate you’ll pay.

For personal loans, most lenders want at least a 600-680 FICO score. For home equity products, you’re looking at 700+ for decent rates, and 720-740+ for the best offers. Bankrate’s pool loan data shows that borrowers with scores above 740 can qualify for rates as low as 5%, while those in the 600s typically see 15% or higher. That gap is real money. On a $60,000 loan over 7 years, the difference between a 7% rate and a 15% rate is roughly $16,000 in additional interest.

HFS Financial’s 2026 pool loan rate data from Q2 2024 shows the spread between loan types clearly: credit union personal loan rates averaged 10.89% on a 3-year term, while 5-year home equity loans averaged 7.13%. That 3.76% difference matters a lot on a large loan.

Two other factors lenders check:

- Debt-to-income ratio (DTI): Most lenders set the ceiling at 43%. Add up your monthly debt payments, divide by your gross monthly income. If you’re over 43%, either pay down some debt first or look for lenders with higher DTI allowances.

- Home equity: For a HELOC or home equity loan, you typically need at least 20% equity in your home. Your lender will order an appraisal to confirm the number.

One tactic worth using: prequalification. Most lenders let you check your likely rate with a soft credit pull, which doesn’t affect your score. Get prequalified with 3-4 lenders before you commit to anything. Also watch for origination fees, which some lenders charge at 1%-8% of the loan amount upfront. A lower APR with a 6% origination fee can end up costing more than a slightly higher APR with no fee.

Step-by-Step: How to Apply for a Pool Loan

Getting from “I want a pool” to “the check cleared” is a 7-step process. Work through it in order, and you’ll avoid the most common delays:

- Get a real contractor quote. Not a ballpark – an actual written estimate that includes all add-ons. Some lenders require this documentation.

- Check your credit score. Free access is available at annualcreditreport.com. Know your number before any lender does.

- Calculate your DTI. Add your monthly debt payments and divide by gross monthly income. If you’re near 43%, you’ll want to know before a lender tells you.

- Decide on your loan type. If you have strong home equity and a 720+ score, home equity loans usually offer better rates. If you don’t want to use your home as collateral, go personal loan.

- Compare at least 3 lenders. Look at APR (not just the rate), term length, origination fees, and whether there’s a prepayment penalty if you want to pay it off early.

- Prequalify with your top choices. Soft pull, no score impact. This gives you real numbers to compare.

- Submit your full application. You’ll need proof of income (W-2s or tax returns), recent pay stubs, and sometimes contractor documentation. Personal loans can be funded in 1-5 business days. Home equity products typically take 2-6 weeks to close.

For a detailed breakdown of what inground projects actually cost by pool type and region – which shapes how much you’ll need to borrow – the inground pool cost breakdown covers the numbers in detail.

Will a Pool Actually Add Value to Your Home?

This is the question homeowners ask when they’re trying to justify the expense. The honest answer: it depends heavily on where you live, but don’t finance a pool primarily as an investment strategy.

On average, a pool adds 1%-7% to a home’s resale value – Zillow puts the number at around 1.5% while Curbio estimates closer to 7%. The regional variation is the real story. Redfin’s analysis of pool value data by market found that a pool in Los Angeles adds an average of $95,393 to property value, while the same pool in Phoenix adds just $11,591. In cold-climate markets like Boston, pools can actually reduce appeal – buyers view them as maintenance burdens rather than amenities.

The typical ROI on installation cost runs 40%-60% recouped at resale. If you spend $65,000 on a pool in a market where it adds $30,000 to your home’s value, you’re not breaking even on the installation cost – but you’ve had years of use out of it.

Finance a pool because you’ll use it heavily for 5 or more years, and the monthly payment fits your budget. Don’t finance one purely on the assumption you’ll recoup the cost at sale. Pools are a lifestyle investment first – treat them that way when you’re running the numbers.

The Bottom Line

Pool loans are a real path to pool ownership for most homeowners. The key is matching the right loan type to your credit profile and financial situation before you apply.

Don’t take the first offer. Compare at least three lenders, check the APR alongside the rate, and watch for origination fees that quietly inflate the total cost. If your credit score is below 700, spending 6-12 months improving it before applying can save thousands in interest. The rate gap between a 650 FICO and a 740 FICO on a $60,000 loan is not small.

Start with your credit score, get a real contractor quote, then use that combination to choose the right loan type. The process is more manageable than most homeowners expect, and the pool doesn’t have to wait as long as you think.

Written by Billy Guteng. May 15, 2026

Billy is a content writer for Kukun. He was born in France, and has lived in multiple cities around the world ever since. He loves art, design and architecture as well as construction and real estate.

Top blog posts

See more >

Recommended

Join our newsletter

Get helpful renovation tips, insightful home maintenance articles, real estate market trends, and more.

Please enter a name

Please enter a valid e-mail