Blog Guides Lending and mortgage

Home Equity Line of Credit vs Personal Loan

Updated Wed, Mar 25, 2026 - 6 min read

Top blog articles

Do you need funding for a major purchase or home improvement project? Fortunately, both personal loans and home equity line of credit (HELOC) can make your financing possible. But if you’re confused between the home equity line of credit vs personal loan, then it’s best to do some research and decide which loan option suits your needs in the best way.

This guide will help you understand both types of loans and their differences. You can make an informed decision before applying for either of the loans.

Want to know about your loan options? Kukun is always happy to help.

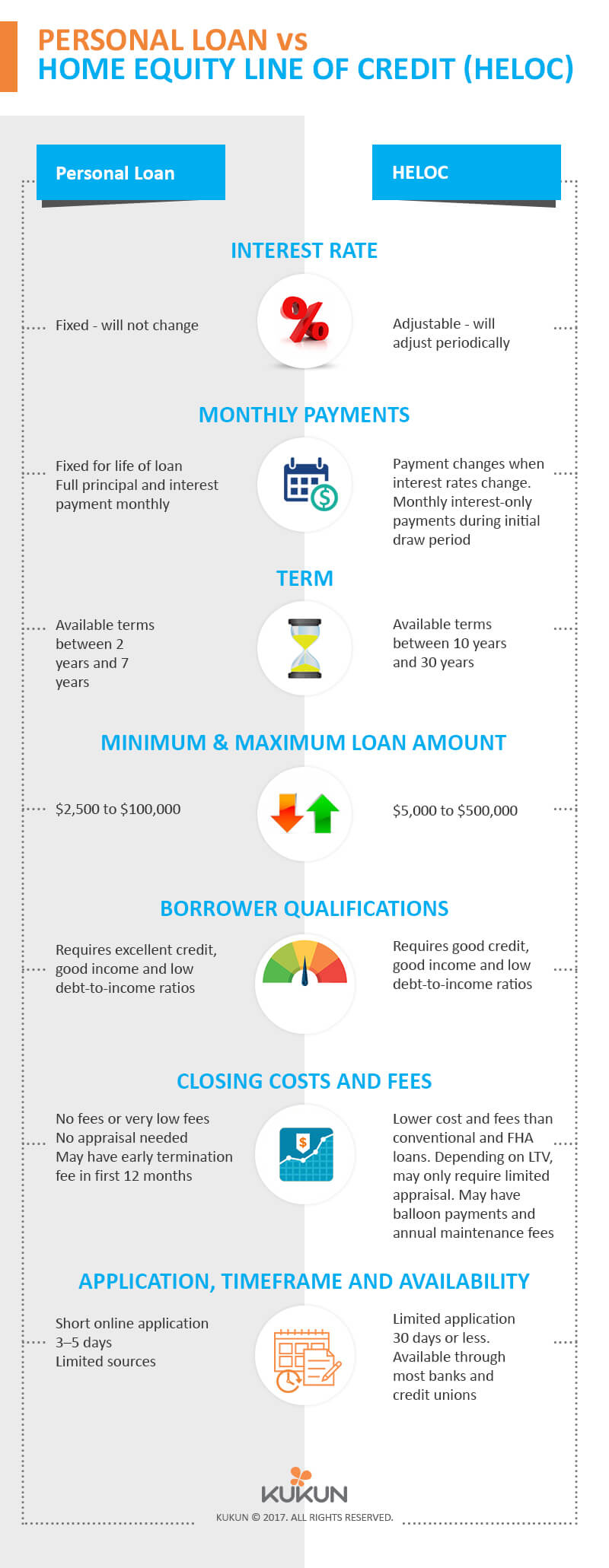

The primary difference in home equity line of credit vs personal loan is that while a personal loan does not typically require collateral, a home equity line of credit loan does. It depends on the amount of your home equity (on calculations based on the difference between what you owe and the value of your property).

What is a HELOC?

Home equity line of credit is similar to a credit card account. You may access your HELOC funds with a debit card or check.

Here too, you may borrow money upon approval, pay down your balance, and access the credit line yet again for a period of time. This period is the draw period, usually of 10 years, whereby you may pay interest-only or minimum payments. Once your draw period ends, the repayment period begins.

So basically in HELOC, you borrow up to your maximum limit, repay the funds, and borrow again if required.

To apply for a HELOC, you need a minimum of 20% equity in your home, a good credit score, and credit history.

What is a personal loan?

A personal loan is also called signature loans as upon qualifying, you can receive the money with just your signature! Basically, you don’t have to put up any assets or collateral for this unsecured loan.

While borrowers in the past used personal loans for credit card debt consolidation or a financial emergency, today, you can use a personal loan for just about anything.

So basically in a personal loan, you borrow a fixed amount of money, repay it at a fixed monthly payment — over a fixed period.

Read more: How to Get First Time Personal Loans (No Credit History)?

Home equity line of credit vs personal loan

Choosing between home equity line of credit and personal loan depends a lot on your situation and requirements. For instance, if you don’t want to use your house as collateral, a personal loan may be better for you. Even if it comes at a higher interest rate.

This is the reason that borrowers prefer personal loans to fund their home improvements, weddings, and other large-scale expenses. Moreover, a personal loan usually offers a quicker way to access cash.

Keep in mind that since this type of unsecured loan is riskier for lenders, the interest rates are usually higher than in a HELOC. But thankfully, personal loan interest rates have become more competitive in recent years. They range from about 6% to 36%. Of course, it depends on the loan amount, length of the loan term, and how good or bad your credit scores are.

Differentiating factors between home equity line of credit and personal loan

A major difference between a personal loan and line of credit is how the borrowed money is paid out. While in the case of a personal loan, it is set and paid out once in a lump sum amount, HELOC sets a credit limit up to which the borrower can take out as much money as required.

Here are some differences that will help you decide the right type of loan for you:

Ease

If you need the cash quickly, applying for a personal loan may be a better option for you than applying for a HELOC. Most offline and online lenders today easily approve a personal loan within a week.

A HELOC, on the other hand, requires a home appraisal and a lengthy approval process, often taking up at least 30 days. Also, qualifying for a HELOC may need you to have a much better credit score than a personal loan.

Interest rates

Interest rates will be better on a personal line of credit vs a personal loan. This is because you’re using your home as collateral. Most funding sources are tempted to give you better rates, especially if you have a lot of equity in your home.

Also, you don’t have to pay interest charges on the amount of the credit line that you haven’t used.

You may even get a mortgage interest tax deduction with HELOC. Which is not the case with a personal loan. Your interest rates start from the moment you get the lump sum amount.

Moreover, a HELOC usually has a variable interest rate, while a personal loan offers a fixed interest rate. This also means that HELOC interest rates can fluctuate over time based on market rates.

Therefore, a HELOC is best if you plan to pay off the loan over a short period of time — before the market interest rates rise. And, if you’re sure to make the repayments on time. Otherwise, any default can lead to possible foreclosure.

Loan terms

A personal loan is also called a term loan as the length of your repayment period and monthly payments are set when you borrow the funds. The repayment terms are typically two years, three years, or five years.

Furthermore, since you have a fixed interest rate, your monthly payments remain the same throughout.

A line of credit, on the other hand, is a revolving credit whereby you can keep borrowing money up till your credit limit. As you pay off the existing debt, you keep replenishing the credit limit.

Here, your minimum payment and overall repayment costs may keep fluctuating — depending on the variable interest rates and on how much of your limit you’ve tapped.

Read more: 5 things you need to know for getting a loan

Which loan is better for you?

Determining which type of loan is better for you depends on your money situation and why and how quickly you need the money. Understanding the difference between both the financial products will go a long way in helping you choose the best financing option.

It’s best to ask yourself whether you want a quick loan with a higher interest rate or wait a bit longer for a loan, but at a lower interest rate.

Home equity line of credit vs personal loan: whichever type of loan you choose, do your research, check the loan terms, length of the loan, and interest rates. And, don’t be afraid to ask your lender as many questions as you need.

Read more: Conventional Cash-Out Refinance Vs HELOC

Written by Kukun staff. December 27, 2017

Home remodeling at its finest. With expertise in all fields involved in nurturing your home, whether is decor, design, construction, or remodel, our team of experts is here to walk you through the process by providing amazing content on a regular basis.

Top blog posts

See more >

Recommended

Join our newsletter

Get helpful renovation tips, insightful home maintenance articles, real estate market trends, and more.

Please enter a name

Please enter a valid e-mail